All Categories

Featured

[/image][=video]

[/video]

This can result in much less advantage for the policyholder compared to the economic gain for the insurer and the agent.: The illustrations and assumptions in advertising and marketing products can be misleading, making the policy seem extra appealing than it may really be.: Realize that economic consultants (or Brokers) earn high payments on IULs, which could affect their suggestions to market you a plan that is not appropriate or in your best interest.

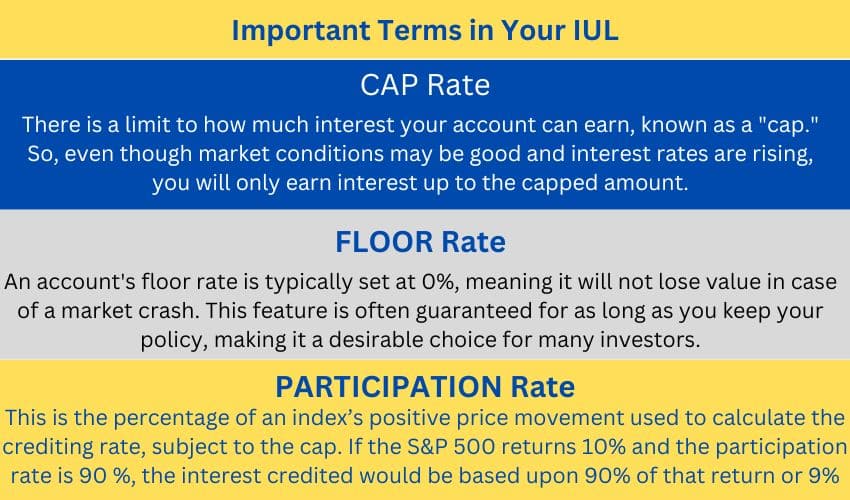

Many account choices within IUL products guarantee one of these limiting variables while allowing the various other to float. One of the most usual account alternative in IUL policies includes a floating yearly rate of interest cap between 5% and 9% in current market conditions and a guaranteed 100% involvement rate. The rate of interest gained equates to the index return if it is much less than the cap yet is topped if the index return exceeds the cap price.

Other account alternatives could consist of a drifting engagement price, such as 50%, without cap, meaning the rate of interest attributed would be half the return of the equity index. A spread account credit scores passion over a drifting "spread rate." If the spread is 6%, the rate of interest credited would certainly be 15% if the index return is 21% yet 0% if the index return is 5%.

Passion is typically attributed on an "annual point-to-point" basis, indicating the gain in the index is computed from the factor the costs entered the account to precisely one year later. All caps and participation prices are then applied, and the resulting interest is credited to the plan. These rates are adjusted yearly and used as the basis for calculating gains for the following year.

Instead, they utilize alternatives to pay the interest promised by the IUL agreement. A phone call option is a monetary agreement that provides the choice purchaser the right, however not the obligation, to get a possession at a specified rate within a certain amount of time. The insurance policy business gets from a financial investment financial institution the right to "acquire the index" if it exceeds a specific degree, understood as the "strike cost."The provider might hedge its capped index responsibility by acquiring a telephone call alternative at a 0% gain strike rate and creating a telephone call option at an 8% gain strike price.

Iule

The budget plan that the insurer has to acquire choices depends upon the return from its basic account. For example, if the provider has $1,000 internet costs after deductions and a 3% return from its basic account, it would allot $970.87 to its basic account to expand to $1,000 by year's end, using the staying $29.13 to acquire choices.

The two biggest variables affecting floating cap and involvement rates are the returns on the insurance coverage firm's general account and market volatility. As returns on these assets have decreased, providers have actually had smaller budgets for buying options, leading to minimized cap and engagement prices.

Carriers commonly illustrate future efficiency based upon the historical efficiency of the index, applying present, non-guaranteed cap and participation prices as a proxy for future performance. Nonetheless, this approach may not be realistic, as historic forecasts usually reflect higher previous rates of interest and think regular caps and involvement rates despite different market conditions.

A far better method could be designating to an uncapped engagement account or a spread account, which involve purchasing reasonably economical options. These methods, however, are much less steady than capped accounts and might call for frequent adjustments by the service provider to reflect market conditions accurately. The narrative that IULs are conservative products supplying equity-like returns is no much longer lasting.

With sensible expectations of options returns and a shrinking budget plan for acquiring alternatives, IULs might supply marginally higher returns than conventional ULs but not equity index returns. Possible purchasers need to run images at 0.5% over the rate of interest attributed to typical ULs to analyze whether the policy is properly funded and with the ability of supplying guaranteed performance.

As a trusted partner, we team up with 63 premier insurance companies, guaranteeing you have access to a diverse series of options. Our solutions are totally free, and our professional advisors give unbiased guidance to assist you locate the very best coverage customized to your needs and budget. Partnering with JRC Insurance Team suggests you get individualized service, competitive prices, and peace of mind understanding your financial future is in capable hands.

Universita Iul

We aided thousands of households with their life insurance needs and we can aid you as well. Professional examined by: High cliff is an accredited life insurance coverage agent and one of the owners of JRC Insurance coverage Group.

In his leisure he takes pleasure in spending quality time with family, taking a trip, and the fantastic outdoors.

Variable plans are financed by National Life and dispersed by Equity Solutions, Inc., Registered Broker/Dealer Affiliate of National Life Insurance Business, One National Life Drive, Montpelier, Vermont 05604. Be sure to ask your monetary consultant regarding the lasting care insurance coverage policy's features, benefits and premiums, and whether the insurance coverage is appropriate for you based on your financial circumstance and purposes. Disability revenue insurance policy typically offers month-to-month revenue advantages when you are incapable to work due to a disabling injury or health problem, as defined in the plan.

Cash value grows in an universal life policy through attributed rate of interest and decreased insurance expenses. If the plan gaps, or is given up, any outstanding superior car loans taken into consideration in the policy plan be subject to ordinary average taxesTax obligations A fixed indexed global life insurance policy (FIUL)plan is a life insurance insurance policy that provides gives the opportunityChance when adequately sufficientlyMoneyed to participate get involved the growth development the market or an index without directly investing spending the market.

{kind=link}

Latest Posts

Index Iul

Index Universal Life Insurance Vs Whole Life

Northwestern Mutual Iul